Untitled Document

In the debate over oil supplies, July 2007 may be seen as a turning point.

The International Energy Agency, a body set up to advise OECD nations on energy

supply and security, broke with its previous optimistic projections of world oil

supply and threw the future of oil into doubt. The IEA’s recently released

“Medium-Term

Oil Market Report” (PDF 1.87MB) reads like a summary of peak oil concerns

made acceptable for the ears of government by occasional disclaimers to the contrary.

However, its central declaration is clear:

Despite four years of high oil prices, this report sees increasing

market tightness beyond 2010, with OPEC spare capacity declining to minimal

levels by 2012 … It is possible that the supply crunch could be deferred

[by decreased demand growth] - but not by much.

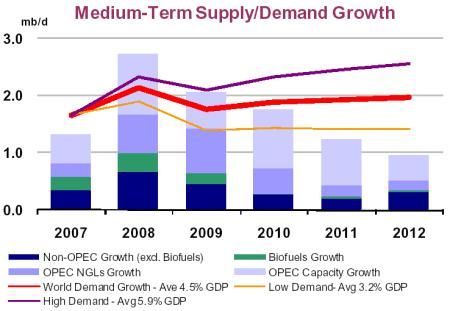

The chart above also shows a number of other interesting points. While considerable

new supply should come on stream in 2008 (and lead to a temporary drop in fuel

prices) there is less optimism for later years. Also, the growth of biofuels,

while significant, is relatively limited. (When examining the chart, remember

the world is currently using about 85 million barrels of oil per day [mb/d].)

It has been the habit of previous Medium Term Reports to assume that the OPEC

nations will raise production to meet any shortfall in growth from non-OPEC

suppliers. However, now this report declares:

Recent history would suggest that a conservative approach to OPEC capacity

is justified.

Despite the declaration of caution, the IEA then makes assumptions of Saudi

Arabian capacity that are not justified by its production performance over the

past few years, including recent times when oil prices have been high and would

reward maximal production.

As illustrated by an insightful comment on the website, www.theoildrum.com,

the IEA assumes current Saudi capacity that is probably over 1mb/d greater than

reality. Saudi Arabia’s declared ability to increase production is very

important in the IEA’s growth projections for the next five years but

in the contrarian peak-oil community there is considerable debate over the truth

behind Saudi Arabia’s claims.

The IEA report is also quite upbeat about new refinery capacity coming online,

especially in the Middle East and China, and the effects this will have on fuel

availability - at least for everything other than shipping (see below). As the

world’s easily extracted oil comes to an end, the "heavier"

(more viscous), more "sour" (higher sulfur) grades remain. This oil

requires greater processing by refineries before it can be used but world refinery

capacity has recently be struggling to cope with demand due to decades of underinvestment.

However, that is now changing:

The refining industry … has responded to market incentives. Investment

in sophisticated refinery capacity is continuing apace … a significant

improvement in refinery flexibility is foreseen.

Interestingly however, this increased refinery capacity shows that every silver-lined

cloud has a black interior. At the moment, shipping uses heavy grade fuel oil

that is cheaper than the lighter grades of oil more suited to gasoline and diesel

fuel production. However, if the capacity exists to refine heavier oil grades

into gasoline then:

The large discounts needed to clear surplus fuel oil production will

become a thing of the past.

... we expect fuel oil markets to tighten significantly in the next

five years. …the new, largely complex refineries will have low fuel

oil yields, and upgrading capacity additions at existing refineries will

further cut fuel oil production.

If this leads shipping to burn lighter fuel grades then the:

… potential for distillate markets to ease over the next five

years would be dwarfed by the impact of [shipping] switching from fuel oil

to distillate.

So increased capacity to refine heavier grades of oil into diesel and gasoline

may ease supply for road transport for a while but may create its own problem

by reducing the oil available to shipping and forcing them to compete for lighter

grade fuels. In fact, it is hard to see how this will not occur if ship transport

is to continue - which it must to support our globalised economy.

The IEA report is also especially notable for the damper it has put on expectations

for growth in natural gas production. The Economist magazine and others have

been optimistic that natural gas might substitute for a large fraction of oil

production. But:

Not only does oil look extremely tight in five years time, but this

coincides with the prospects of even tighter natural gas markets at the

turn of the decade. … it is abundantly clear that if the path of demand

does not change on its own, it may well be driven to change by higher prices.

In other words, prices of oil and gas will rise until sufficient demand is

destroyed to keep them in balance with supply.

The IEA and peak oil

The IEA report is refreshingly explicit on the dwindling production from older

fields and the peak oil idea:

Net oilfield decline rates average 4.6 per cent annually for non-OPEC

and 3.2 per cent per year for OPEC crude. … All told, the forecast

suggests the industry needs to generate 3.0mb/d of new supply each year

just to offset decline.

But, unlike those who support the “peak oil” theory, the IEA is

unwilling to give primacy to oilfield decline as the major factor determining

the volume of oil produced over the next five years:

… Hydrocarbon resources are finite, nonetheless issues of access

to reserves, prevailing investment regime and availability of upstream infrastructure

and capital seem greater barriers to medium-term growth than limits to the

resource base itself.

So the IEA sees geopolitical problems (for example, resource nationalism),

escalating project costs and, especially, “slippage” (delays) in

project completions as being more important in restricting oil production than

decreasing oil production from maturing fields.

When talking about oil production in non-OPEC nations, the report admits that

conventional crude oil production from these nations is declining and is only

maintained at current levels by new, non-conventional sources of oil. However,

the IEA then attempts (rather unconvincingly) to avoid declaring that non-OPEC

oil production has peaked by saying that the definition of what is “conventional”

crude oil changes with time:

Certainly our forecast suggests that the non-OPEC, conventional crude

component of global production appears, for now, to have reached an effective

plateau, rather than a peak. ... While there might be a temptation to extrapolate

this trend, citing a peak in conventional oil output, a degree of caution

is in order. Firstly, the concept of “conventional” oil changes

with time, technology and economics.

OPEC is expected to provide an additional 4mb/d of crude oil by 2012, an increase

of over 11 per cent from this year (and almost half of this increase is expected

to come from Saudi Arabia which has recently shown falls in production - see

also the preceding comment on Saudi Arabia).

Other points of interest in the report

Growing demand from China and other developing nations will be the central

cause of “market tightness”:

The main driver of demand growth in Asia will be China ... Given the

country’s booming economy, oil product demand is projected to increase

by 5.6 per cent per year on average … roughly a quarter of the world’s

annual demand increase.

But India’s role in the oil market is overestimated:

It is worth emphasising that, despite the similar size of their populations,

India and China are not in the same league with regards to oil demand. The

frequently quoted concept of “Chindia” is misleading: India’s

demand will barely represent a third of China’s by 2012.

The report speaks surprisingly frequently of delays in both oilfield development

and refinery construction due to a number of factors. For example, when forecasting

production from new projects in non-OPEC nations, the report states:

Slippage varies between two and 36 months, but is typically around

six months … shortages of labour, raw materials, fabrication and drilling

capacity and transport infrastructure may continue to undermine output growth

for some time.

The report is also notable for its pessimism (i.e. realism) about the potential

of biofuels. The report’s authors sound very similar to peak oil advocates

when warning of the potential for biofuel production to raise food prices and

the effects this will have on poorer nations:

Such a lifting of agricultural prices could have far-reaching global

economic effects - even excluding the moral issues related to food supply

…

… The International Monetary Fund (IMF) warned in a recent report

that global food prices had risen by 10 per cent in 2006, in part due to

higher US demand for corn (for ethanol production). Demonstrations against

higher corn prices were reported in Mexico, where it is a staple of the

national diet.

… There are similar worries about the environmental impact of

biofuels. Hailed by some as an easy way to limit carbon emissions, others

have pointed at the scope for environmental damage. … forests are

being razed for feedstock plantations, offsetting potential gains through

carbon capture. … In many countries there is concern that increased

corn production will put a significant strain on available water.

Concluding remarks

The IEA Medium Term Market Report is 82 pages long and contains much more

of interest than I have summarised here.

The most pessimistic supporters of peak oil believe that decline of

total world oil production is imminent. Indeed, I previously described how major

figures in the industry such as energy investment banker Matt Simmons, oil entrepreneur

T. Boone Pickens and retired National Iranian Oil Company Vice-President Ali

Samsam Bakhtiari believe we are now at peak.

Nevertheless, the IEA Medium Term Report is refreshingly open and balanced

in its approach to this most vital of topics. It is a further nail in the coffin

for the irresponsibly optimistic future oil production scenarios painted by

industry cheerleader Cambridge Energy Research Associates and the biggest of

Big Oil - ExxonMobil. The publication of the IEA report means that the writing

is now on the wall for all governments and industry to see.

Much higher oil prices can be expected within five years at best. Before

this, a short, but deceptive, fall in oil prices may occur in 2008-9. It remains

to be seen whether the political courage exists to openly discuss this issue

and begin the painful process of weaning ourselves off oil. I am not optimistic.

_______________________________

Read from Looking Glass News

Threats

of Peak Oil to the Global Food Supply

Peak Oil

Happened on 12/16/2005...

Peak Oil

= Urban Ruin

The Peak

Oil Crisis: A Mid-Summer Review

"Peak

oil" determined to strike inside U.S.: Yet another memo that Bush didn't

read

Peak Oil

and the End of Empire

Prepare

for Peak Oil Now

Peak Oil:

What We Know Now

Peak

Oil and the working class

THE

END OF THE AGE OF OIL